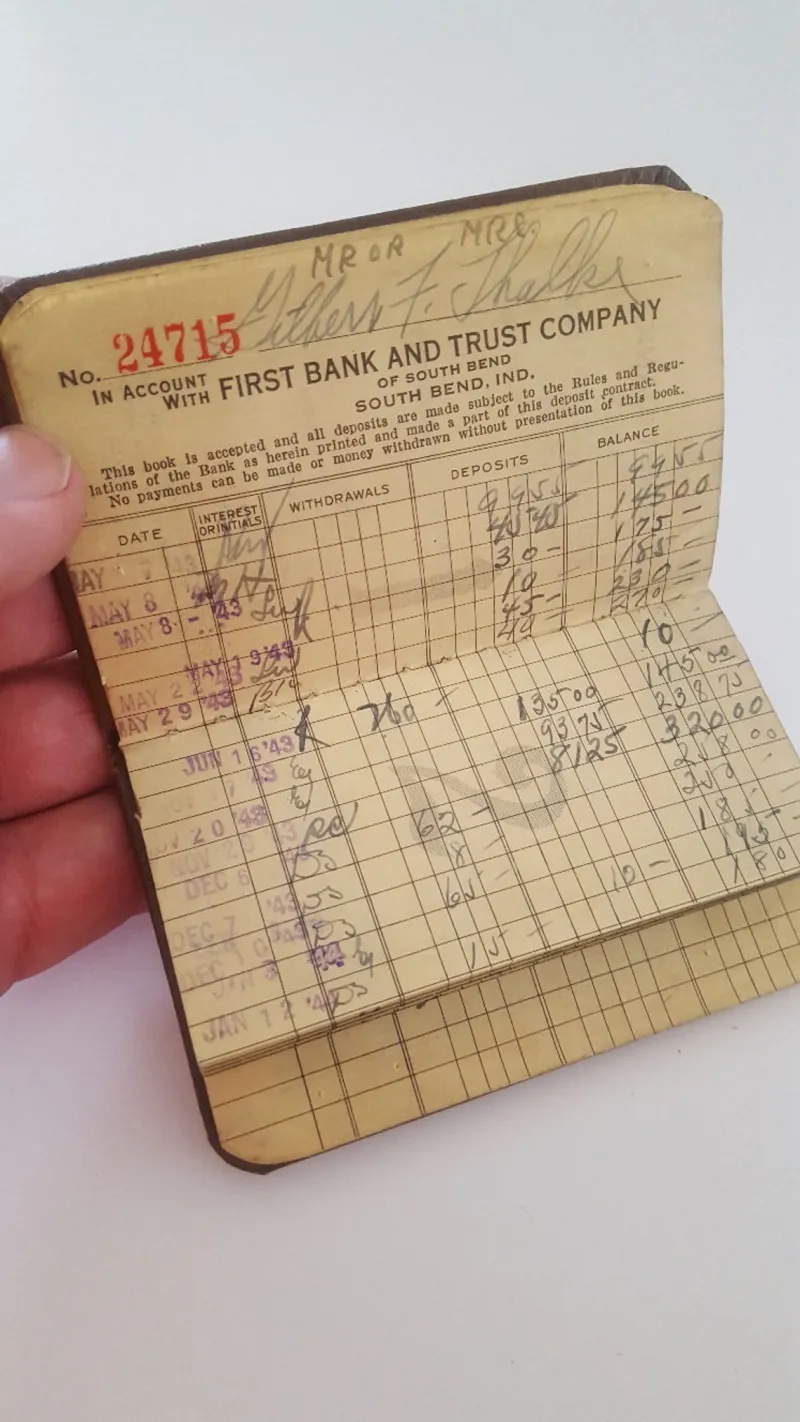

Somewhere in a drawer in your grandparents' house, there might still be one: a small, narrow booklet with a fabric or paper cover, stamped with the name of a bank that probably no longer exists. Each deposit and withdrawal recorded by hand in neat columns. A running balance in blue ink. An interest rate printed on the inside cover that, by today's standards, looks like a typo.

The passbook savings account was, for several decades of American life, the foundational tool of personal financial stability. It wasn't complicated. It didn't require a financial advisor, a risk tolerance questionnaire, or an understanding of expense ratios. You put money in. The bank paid you to keep it there. The balance grew. That was the entire system.

For millions of ordinary American households, it was enough.

What the Mid-Century Savings Culture Actually Looked Like

The postwar savings culture in the United States wasn't just a habit — it was an expectation, reinforced by institutions, by schools, and by the lived experience of a generation that had watched the Depression strip families of everything they hadn't managed to set aside.

Commercial banks offered passbook savings accounts with interest rates that, through much of the 1950s and 1960s, ranged from 3 to 5 percent annually. That number sounds modest until you compare it to the near-zero rates that defined the post-2008 era — or the current environment where many basic savings accounts still pay fractions of a percent despite a dramatically higher federal funds rate. In the mid-century context, a family that consistently deposited even a modest portion of their income into a passbook account was genuinely building something.

U.S. savings bonds occupied a parallel lane in the culture. Series E bonds, introduced during World War II, became a fixture of civilian financial life long after the war ended. They were given as birthday gifts, distributed as Christmas bonuses, and purchased at the post office by people who had no other relationship with the financial system. The concept was simple: you paid less than face value, waited the maturity period, and collected the difference. No brokerage account required. No minimum balance. No fees.

Schools in many states ran savings programs in partnership with local banks, where children could bring in small deposits on designated days and receive stamped passbooks of their own. The lesson wasn't just financial — it was cultural. Saving was something ordinary people did as a matter of course, not something that required access to sophisticated products or professional guidance.

The Regulatory Architecture Behind the Simplicity

The simplicity of mid-century savings wasn't accidental. It was partly the product of regulatory frameworks put in place specifically to make banking accessible and predictable for ordinary households.

Regulation Q, a Depression-era rule that capped the interest rates banks could pay on deposits, created a stable and somewhat artificial environment where savings accounts were straightforward instruments. The cap meant banks couldn't compete aggressively on rates, which in turn meant the savings account remained a plain, standardized product rather than one element in an increasingly complex menu of financial options.

The deregulation of interest rates in the early 1980s was intended to help savers by allowing banks to offer market-rate returns. In practice, it contributed to the fragmentation of the savings landscape. Money market accounts, certificates of deposit with varying terms, and eventually an explosion of investment products began to compete for the dollars that had once simply sat in passbook accounts. The simplicity that had made saving accessible started to erode.

When the Complexity Became the Product

The shift from saving to investing as the primary vehicle for wealth-building didn't happen in a vacuum. The decline of defined-benefit pensions through the 1980s and the rise of the 401(k) system transferred retirement savings responsibility from employers to employees — and in doing so, required ordinary people to engage with financial markets whether they wanted to or not.

Suddenly, the question wasn't just "how much should I save?" It was "what should I invest in, across which asset classes, with what fee structure, rebalanced on what schedule?" These are not intuitive questions for someone whose parents had a passbook and a savings bond tucked in the kitchen drawer.

Financial literacy became a growth industry, which is itself a sign of how much complexity had been introduced. When saving was simple, you didn't need a podcast to explain it. When it became a matter of navigating target-date funds, Roth conversions, and the difference between a traditional IRA and a brokerage account, the barrier to entry rose significantly — and it rose unevenly. Households with professional networks, college educations, and exposure to financial planning had better odds of navigating the new system. Those without those advantages were more likely to disengage, defer, or make costly mistakes.

What the Numbers Reflect

The personal savings rate in the United States hovered between 10 and 17 percent through much of the 1970s. By the mid-2000s, it had dropped below 3 percent. It spiked during the pandemic as a product of forced reduced spending and stimulus deposits, then fell again as inflation eroded purchasing power and the cost of basic living consumed more of household income.

Financial anxiety is now a persistent feature of American life across a surprisingly wide income range. Surveys consistently find that a majority of Americans couldn't cover a $1,000 emergency expense from savings without borrowing. That's not purely a product of stagnant wages or rising costs — though both are real. It's also a reflection of a savings culture that has been systematically complicated, and in being complicated, has become less accessible.

The Simple Idea That Got Lost

The passbook account represented a specific promise: that ordinary people, doing ordinary things with their money, could build genuine stability over time. The bank would pay them for the privilege of holding their deposits. The math would work in their favor without requiring them to become amateur portfolio managers.

That promise didn't disappear because it was a bad idea. It disappeared because the financial system evolved in directions that made it less profitable to offer. What replaced it is more sophisticated, more flexible, and — for people with the knowledge to navigate it — potentially more rewarding. But it is not simpler. And for a significant portion of the American population, the complexity itself has become the obstacle.

The passbook was a small book with a big idea inside it. We replaced it with something more powerful and far harder to use — and then were surprised when fewer people saved.